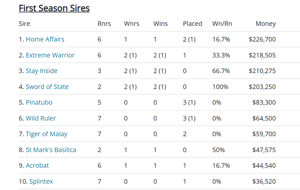

To take advantage of the generous Small Business Capital Gains Tax (CGT) concessions, one of the main criteria is that the asset must be an “active asset”.

![]()

What is little known though is that an asset that is only partly used for business can still be an active asset. This is because the definition of an active asset does not require that the asset is 100% used for business purposes.

As long as the asset is used in the course of carrying on a business, it will still be an active asset, even though the asset may have a small business use percentage (e.g., 10%) and a large private use percentage (90%).

Of relevance to industry players, one of the most common types of assets that is used partly for business and partly for private purpose is a farming/breeding property. This presents an exciting opportunity for breeders to use these CGT concessions in circumstances where they thought they would be excluded.

1,0 Active asset overview — used in a business

As part of its definition, a CGT asset is an “active asset” of a taxpayer at a given time if, at that time:

“the taxpayer owns the asset (whether tangible or intangible) and it is used, or held ready for use, in the course of carrying on a business that is carried on (whether alone or in partnership) by the taxpayer, the taxpayer’s affiliate or another entity connected with the taxpayer”

Example 1 – Active asset example

Rocco ran a small business printing leaflets for environmental causes. He purchased a printing press in February 2000. He upgraded to a computer system in November 2005, at which time he sold the printing press. The printing press had been used exclusively in his business for the entire period. The printing press satisfies the active asset test.

But...what if the asset is partly used for private purposes, can that asset still be an “active asset”?

Example 2 – Asset part used for business

Georgie is a horse breeder who carries on a business of horse breeding from her 100-acre farming property. The horse breeding occupies approximately 20% of the farm, the balance of the farm is used for private purposes.

In search for a larger farm for her business, Georgie sells her farm and enters into a contract to acquire a larger property. The sale generates a capital gain, and Georgie wants to take advantage of the small business 50% reduction and retirement exemption.

Georgie’s farm will qualify as an “active asset” under the CGT rules as it was used “in the course of carrying on a business”, even though only in part. Therefore, Georgie will be able to apply the above small business CGT concessions (provided all other relevant conditions are met).

It should be noted that these concessions are applied (to the capital gain remaining) after applying the main residence exemption and the 50% CGT discount (if the property held for at least 12 months).

“Used in the course of”

There is a recent tax case that supports the above findings that an asset “part used” for business will qualify for the small business GGT concessions.

The CGT laws require the asset to be used “in the course of carrying on a business”. That phrase was discussed at length in a 2020 Full Federal Court decision and in the proceedings that had led up to that decision. In that case the taxpayer, who carried on a business of building, bricklaying and paving, purchased land next door to his family home and used it to store work tools, equipment and materials. The land had sheds, high walls and a gate to secure the property. Work vehicles and trailers were parked on the property, and tools and items were collected from there on a daily basis.

The full court held that the secure storage of the tools and materials of the taxpayer's business on a daily basis was very much part of the course of the carrying on of that business. In so holding, the court unanimously overturned another decision and the view that, in order for an asset to be used “in” the course of carrying on a business, it was necessary for the use to have a direct functional relevance to the carrying on of the normal day-to-day activities of the business that were directed to the gaining or production of assessable income.

2.0 Active asset — used in a business carried on by someone other than the taxpayer

If your breeding business is operated from a property owned by a “connected” entity, that property can still qualify for te small business CGT concessions. The common example is if the breeding business is run in one entity, yet the property on which the business is conducted, is held in another.

The definition of “active asset” operates such that a CGT asset leased by a taxpayer (or otherwise made available) to a connected entity for use in the connected entity’s business is an active asset of the taxpayer unless relevant exclusions apply.

|

Example 3 – property owned by a connected entity |

|

Peter runs a breeding business through a company of which he is sole shareholder and director. Michael also owns the property from which the breeding business operates via a related “connected” trust. As Peter’s company and trust qualify as connected entities, the breeding property is an active asset of Peter’s. That is because it is used in the course of carrying on a business by an entity connected with Peter. |

Please do not hesitate to contact the writer if you wish for me to clarify or expand on any of the matters raised in this article.

PAUL CARRAZZO CA

CARRAZZO CONSULTING PTY LTD

801 Glenferrie Road, Hawthorn, VIC, 3122

TEL: (03) 9982 1000

FAX: (03) 9329 8355

MOB: 0417 549 347

E-mail: paul.carrazzo@carrazzo.com.au

Web: www.carrazzo.com.au